PDIA in Sri Lanka: Attracting Anchor Investors in Solar Panel Manufacturing

What It’s Like Working as a Research Fellow at the Growth Lab

CID’s Growth Lab is a dynamic program driven by faculty, fellows, and research assistants who are seeking to understand the facets of economic development and to uncover how countries, regions, and cities can move into more productive activities. Our Research Fellows are integral to the success of the Growth Lab: the role’s responsibilities range from research in Cambridge to field work across the globe, and interactions with government officials.

Led by Ricardo Hausmann and a diverse, interdisciplinary team of research fellows, our work takes us around the world. Current projects include Albania, Ethiopia, Mexico, Saudi Arabia, and Venezuela.

Tim Cheston, Semiray Kasoolu, Shreyas Matha, Ljubica Nedelkoska, Miguel Santos, and Nikita Taniparti share their perspectives on the role of a Research Fellow.

What led you to CID’s Growth Lab? Why did you want to work here?

Shreyas Matha: After graduating with my masters, I was looking to work at a place that addresses public policy questions but did not restrict itself solely to techniques in traditional economics. What appealed to me most about working at the Growth Lab was that the place is open to embracing experiments in newer techniques such as natural language processing and machine learning.

Semiray Kasoolu: The Growth Lab is a place of independent thinkers who are not afraid to use a holistic methodology to diagnose different development problems. And to me that freedom of research meant a lot. Another thing that really impressed me was the efficiency of deployment of those research findings to developing countries and to the counterparts in those countries. And that also really impressed me because that is very different from what I know about other development institutions.

What stands out about the Fellows role at the Growth Lab? What is your level of engagement with policymakers?

Tim Cheston: The fellows really are the front line of applying these ideas in the field, and they have a range of expertise and specialties and analyzing different data sets and applying them to different policy purposes. Traveling to Colombia, Mexico, Indonesia, Saudi Arabia and Ethiopia, and working hand in hand with ministers and technical staff across all of those countries has been a real privilege, to see both the larger struggles that unite all of those countries but also the unique features of each one of those places.

SK: The role of a fellow at the Growth Lab is unique in that it combines three things. One is using quantitative methods to discover and probe for development problems. The second one is to validate those with field work and field trips. And the third one is to use those the first two to come up with policy implications and inform of policy work.

Ljubica Nedeloska: I had the opportunity to engage with policymakers on both the technical level and the policymaking level and also on a variety of issues such as employment strategy, disapora relations, fiscal projections, employment projections, fiscal policy among other things. This experience gave me a very interesting chance to see inside how governments work. And I think this is very unique to the GL and I don’t think it would have been possible to learn if I would have stayed in solely academia.

Nikita Taniparti: You’re doing research–you’re reframing the way that governments and policy makers ask questions… You get to interact with the minister or the government, and you hear why they can’t just do the easiest policy option that you might think they should be doing.

What is your favorite part about working at the Growth Lab?

LN: What I like most about working at the Growth Lab is the interdisciplinary teams of highly motivated and highly talented fellows. I also enjoy working with some of the most brilliant minds in the field of economic development. This place has high energy and also high optimism which I enjoyed very much. And last but very important, I recently became a mom and the Growth Lab specifically offered very reasonable conditions for work/life balance.

SM: I’d say my favorite part about working at the Growth Lab is that I get to work with a floor full of postdocs and Ph.D. students who are all interested in working on questions in public policy but also coming at them from new and interesting perspectives.

NT: The Growth Lab is where you get this chance to use your intellectual curiosity to ask the questions that really matter. You’re not just working on a really small part of something where you don’t know the outcome. Our research questions that can be very theoretical are all driven by something that’s happening in the world. We know exactly who we’re working for, whether it’s farmers on the ground or foreign workers in a different country. You know why you’re asking the question and why you’re asking it the way you do.

Miguel Santos: I like arriving in a location you know very little about, with a team of highly qualified people that challenge you constantly, and gradually learning about that place. This process of learning the nuances of a country and translating that into policy, and having the capacity to surprise people who have been there a long time, that’s my favorite part of the job.

This Q&A was edited for clarity and brevity.

What It’s Like Working as a Research Assistant at the Growth Lab

Harvard’s Growth Lab is a bustling hub of faculty, fellows and staff working to understand the dynamics of economic growth and uncover how countries, regions, and cities can move into more productive activities.

Led by Ricardo Hausmann and a diverse, interdisciplinary team of research fellows, our work takes us around the world. Current projects include Albania, Ethiopia, Mexico, Saudi Arabia, Sri Lanka, and Venezuela.

Research Assistants also play a fundamental role on our team. Not only do they provide research support by analyzing and managing datasets, they also collaborate with our high-level counterparts, offering comparative analysis of policies.

Three current RAs Sehar Noor, Bruno Zuccolo, and Ana Grisanti share their perspectives on what makes the position unique.

What led you to CID’s Growth Lab? Why did you want to work here?

Sehar Noor: CID is really at the frontier of a lot of the topics that I was interested in as an Economics major in undergrad. Everything from growth diagnostics to complexity work, it’s looking at diversification from a unique perspective, and I was drawn to both the faculty and the research that is produced by the fellows here.

Bruno Zuccolo: What I really liked about the Growth Lab was the intersection of researchers working on the very academic side of learning about growth, but also a very dedicated team of fellows and research assistants applying that research in country projects. The country projects are varied and work through very different economies; when I first joined I was working on projects in Albania and Argentina, and I was working on issues of growth in all those countries. I think this was a fantastic opportunity to learn about countries that I didn’t know that much about and to be able to apply rigorous methodology and statistical analysis.

What stands out about the Research Assistant role at the Growth Lab?

Ana Grisanti: I have many responsibilities, ranging from data cleaning and the visualization of the data, to finding out who we want to interview in the field and going into the field and engaging in interviews with counterparts. One of the states within Mexico that we were working on was Baja, California, and we were doing a growth diagnostics and complexity analysis in the state. The second time I traveled to Baja, I had the opportunity to present our findings to our counterparts, which was a thrilling experience for me. I think that’s unique for the RA position at CID and one I would not have at any other center.

BZ: What I like about being an RA at CID’s Growth Lab is that you’re working on multiple projects at once, and that means you get to explore a lot of issues specific to each country. So in Albania, where I’ve worked for the past year, we work on issues of agriculture, macro growth, trade, and tourism, and as an RA you don’t always get the opportunity to delve into as many issues as this. The other thing about being an RA that’s fantastic is going to the field. At CID, the RAs really travel and represent the whole of CID in meetings with high level government officials. I remember during my second trip to Albania, we met with several of the Ministers, and I had one-on-one meetings with high level officials in the Ministry of Finance, and that’s just a unique opportunity that I couldn’t imagine having anywhere else.

What is your favorite part about working at CID’s Growth Lab?

SN: I think my favorite part is definitely the people. You have postdocs, fellows, and developers who are experts in their fields and so generous with their time. They make sure that I’m not just getting my work done, but that I’m also building skills that I can use in my future. I think it’s a place where people invest in you, and it’s not just for that deadline or for that project, but in the long run.

BZ: What I’ve most enjoyed about working at CID is how much I’ve learned while applying all of it to concrete policies in the countries we work in. I’ve learned numerous statistical methods, I’ve learned how to code in computer languages, I’ve learned how to work with the counterparts.

AG: This can be a cliché, but my favorite part about working at CID is the people and the attitude that everyone has toward the work. Everyone is willing to help when you have questions or ideas that you think are worth exploring. I can confidently say that I’ve made a lot of great friends here.

Email us at growthlab@hks.harvard.edu if you’re interested in becoming a Research Assistant at the Growth Lab and visit our Jobs page for a list of available opportunities.

This Q&A was edited for clarity and brevity.

The Case for the Albanian Investment Corporation

Re-visiting the “Sector Targeting” study: Assessing the study’s impact

Author: Neluni Tillekeratne, Sri Lanka Project Officer

Part 2: Assessing the impact of the report compiled by the “Sector Targeting Team”

Just over one and a half years ago, Sri Lanka’s Board of Investment (BOI) and Export Development Board (EDB) collaborated with the Center for International Development at Harvard University (CID) to study economic sectors for their investment and export potential.

Twenty officials from the BOI and EDB formed a “Sector Targeting Team” (or “T-Team”). The team assessed 30 sectors – all tradable activities (goods and services) of the private sector – and finally ranked their top sectors for investment and recommended strategies for promoting them. Using the Problem Driven Iterative Adaptation (PDIA) approach of CID’s Building State Capability program, the T-Team met weekly, working continuously over a three-month period. The resulting study represents the hard work of these dedicated government officials.

The previous post described the methodology of this study. It explored the numerous stages in which raw data across multiple indicators was analyzed, ultimately deriving a final list of subsectors with the highest potential of succeeding in the export market as products from Sri Lanka.

This post will explore if this detailed research effort went on to catalyze impact in Sri Lanka’s efforts towards export-promotion.

The team shared that despite the study being released just a short while back, it has impacted BOI across multiple tiers of strategy, action and influence. In particular, they described how the study has catalyzed impact in 8 different ways.

To document the tangible outcomes that emerged as a result of this study, I met with the lead authors (and beneficiaries) of this research initiative at the BOI: Mrs Champika Malalgoda (Executive Director, Research and Policy Advocacy), Mrs Priyanka Samaraweera (Director, Research and Policy Advocacy), and Mrs Ganga Palaketiya (Deputy Director, Research).

The team shared that despite the study being released just a short while back, it has impacted BOI across multiple tiers of strategy, action and influence. In particular, they described how the study has catalyzed impact in 8 different ways.

1. Informed strategy

Strategies derived from the BOI-EDB-Harvard study were incorporated into the BOI 2017-2020 corporate plan. The document, also known as the strategic plan, defines key targets for the institution, specifically in terms of:

- stating the BOI’s broad objectives and strategies,

- setting specific targets such as for FDI, exports, employment creation, export as a percentage of national GDP,

- identifying countries to focus on, in terms of top sources of outward investments, counties who have come to the region, and how we could approach them.

Mrs Malalgoda commended the corporate plan as the most comprehensive in the recent history of BOI, in part due to its identification of “target sectors”. The BOI focused on the top sectors recommended in the BOI-EDB-CID study, since the report predicted a high probability of returns for the investment of effort and time into these specific sectors.

2. Renewed plan of action

Given that the new corporate plan altered routine strategies of the BOI, the action plan of the institution was also revised. BOI incorporated new activities based on recommendations made by the BOI-EDB-Harvard study. The new action plan actively pursued the potential of target sectors.

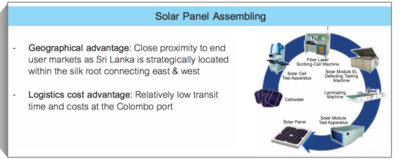

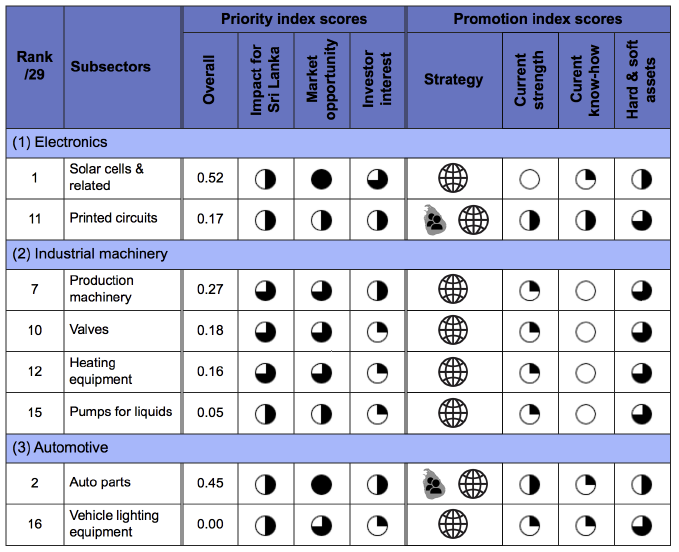

The team immediately took to studying the top sectors. Mrs.Ganga was an active member of a team which acted on requirements of the action plan. Out of the identified sectors, “Electronics”, suggested “solar panels” as the highest scoring sub-sector with the highest potential of attracting a foreign investor (see figure 5).

The team identified the solar panels sector as a target sector, it was actively explored as an option by the Investor Engagement Team (I-Team). The I-Team was set up to specifically study the potential of solar panel manufacturing and other promising sectors, create pitch books, and promote the potential of the sectors to foreign investors. The team immersed themselves in practical study methods including, site visits and meeting with potential/past investors to understand the exact process through which an investor could be convinced and supported to launch a solar manufacturing initiative in SL through an FDI.

3. Reforming outdated policies

The implementation team discovered a significant number of challenges when navigating policies which governed the process of facilitating FDI and so the BOI attempted to advocate for new policies which accommodated interests of the investor and the government. Coordination with the top levels of the government helped the team secure approvals to change policies.

4. Securing investment for the “Solar panel” sector.

Investor confidence was increased as a result of such efforts. The team was ultimately responded to by one of the largest solar manufacturers in the world. Negotiations are currently underway for an FDI with this – a reward for months of dedication.

The investment was secured as a result of the team investing 6 months to study the sector. The pitch books created through the process proved to be a success.

The success of pitch books has encouraged the government to train 40 officials (from BOI and EDB) to be specialists in 10 more sectors, in hopes of finding the same success enjoyed by the I-Team in securing a much needed FDI for the country. The pitch books will be distributed to Sri Lankan Embassies and multinational companies who could potentially invest in Sri Lanka.

5. Ensuring oversight of a Coordinating Committees

A common challenge in the government structure is the existence of multiple ministries and line-agencies whose functions overlap each other. When coordinating with these agencies, 36 line agencies were identified in the process of approving all grants needed to secure an FDI for the solar sector with each line agency needing up to 12 approvals. The process is a constraint which discourages interested investors. The T-Team addressed the clear need for a coordinating committee to overlook and administer the approvals process by facilitating the formation of a committee to coordinate line agencies, in January this year.

“The study shows the need for exports and investments to be a national endeavour with multiple stakeholders in different tiers of investor promotion” – Mrs. Champika Malalgoda

6. Informing Sri Lanka’s National Export Strategy

Mrs Malalgoda shared that the prioritization of sectors suggested in the report was used to support the formulation of the recently launched National Export Strategy (NES) of the EDB. The integration of research into initiatives across the government is an example of knowledge sharing across institutions.

7. Facilitating the launch of new industrial zones in SL for the first time in 15 years

The BOI even addressed crucial bottlenecks in FDI promotion, especially the availability of land for industrial zones. Mrs Priyanka Samaraweera was part of the land team which set out to understand the issues around the lack of suitable land for new manufacturing plants. The following success story of the land team was shared as one of the most rewarding results of the T-Team report.

“Access to land for new ventures is considered a bottleneck in the process of securing investor confidence. More than 80% of land in the country is owned by the government, and the government’s export processing zones are for the most part fully occupied; as a result, interested investors often turn away due to the lack of suitable industrial locations. To further understand the land constraints, an L-Team (land team), engaged in a research exercise. They compiled a comprehensive database on potential plots of land which could be used as Industrial zones. The team conducted a land analysis and matched the available facilities in vacant plots of land, to the specifications required by an investor of a targeted sector, with the preliminary analysis assessing over 80 plots of land.

It was interesting to note that when ideal requirements for an industrial zone were assessed, the newly identified lands offered conditions comparable to the BOI’s existing zones such as in Katunayke and Biyagama. Finally, 25 lands were identified as potential industrial zones” – Mrs. Priyanka Samaraweera

Three lands have now been identified by the government to be developed into industrial zones, including Mawathagama, Bingiriya and Milleniya, an initiative by the government for the first time in over 15 years. This is one of the most impactful results of the study. This progress is a direct result of the BOI-CID study. Coordination toward establishing a new industrial zone improved through the identification of new sectors through the study.

Will this impact continue to multiply?

Mrs. Malalgoda believes the study will go on to inform a policy framework which will support new zones. The policy will be designed to maximize the output and facilitate efficient administration of each zone.

“The final outcome is a rich resource in which any potential investor, researcher, or another interested party can obtain over sixty data points on any sector, as well as aggregated index scores for six major factors. We also hope that by providing access to this research, it may serve as a model for other economic development institutions as well.” – Mrs. Champika Malalgoda

A number of institutions supported the hard-working team at the BOI including the Department of Census and Statics and the Department of Customs who provided in-depth, high-quality data to support the research initiative. The report informed many stakeholders who work towards a common goal of reviving the Sri Lankan economy. We look forward to visiting this team again in a year or so, to hear more stories of the impact of the T-Team report.

“I have realized why by observing this team in Sri Lanka: they are more committed to the work than any outside consultant I have ever seen (because it is their country, and the result of today’s diversification efforts will have a huge impact on the team members’ children) and bring vital contextual know- how to the job better than any outside consultant” – Matt Andrews, Senior Lecturer in International Development, Harvard Kennedy School Faculty Associate, Harvard Center for International Development

Re-visiting the “Sector Targeting” study: Why BOI and EDB opted for sector targeting

Agritourism in Albania: Trends, Constraints, and Recommendations

Working with the Sri Lankan Tourism Development Authority to Develop Resources for Creating and Analyzing Tourism Policy

Author: Ceylan Oymak, HKS MPP Student

Sri Lanka tends to conjure up a range of ideas by would-be tourists: its deeply intriguing history and relation to colonial powers, a 26-year civil-war with the Tamil Tigers, or, more simply, the paradisiac beaches, beautiful landscape, warmth of the people and the rich cuisine. I believe each of these things contribute differently to Sri Lanka becoming one of world’s top tourist destinations in the past few years.

High demand among foreigners to visit Sri Lanka surely presents wide opportunities for the country’s growing economy, while also revealing certain constraints for further development. Tourism is the third largest source of foreign currency into the Sri Lankan economy. However, the industry still does not live up to its full potential when compared with other countries offering similar experiences. Currently, the Sri Lanka Tourism Development Authority (SLTDA) is working with donor organizations, external consultants and development specialists to achieve a set goals laid out in the 2020 Strategic Tourism Plan, in order for Sri Lankan tourism to overcome the existing barriers to growth.

The overarching aims of SLTDA included in the Strategic Plan are 1) Increasing coordination in tourism between public and private sector organizations, 2) Improving the tourist experience and moving away from being known as a ‘cheap’ tourist destination, and 3) Expanding the technical capacity to gather and analyze data in order to better understand tourists’ preferences and patterns as they navigate the country and accurately quantify the contributions of tourism the overall economy.

I felt very lucky to be working at SLTDA for 10 weeks during the summer of 2018, where projects and proposals falling under these overarching goals were being drafted or implemented in a strict timeline in order to fulfill the plan set out for 2020. The most valuable part of my experience of working with SLTDA was that it captured different aspects of the ongoing work as I spent some time working with different people who come from various backgrounds, with different interests.

During the first two weeks, I was involved in the negotiations procedure for a large loan they are expecting to receive by next year for investing in tourism-related infrastructure and skill development in the hospitality sector. The loan will be invested in projects at the provincial level according to the needs and capacities of each of the province(s) the donor organization chooses (Note: Sri Lanka is divided into nine provinces where each province is represented by a local administrative government). These two weeks allowed me to gain exposure to the work needed to done on the ‘receiving end’ of a donor loan. Furthermore, as I attended the presentations of regional councils who are in a way competing for the loans, it further exposed me to the natural and cultural diversity of Sri Lanka and the variety of experiences it can offer to foreigners.

Another ongoing area of work was to review and edit the SLTDA Statistical Reports – which are geared towards policy-makers and other entities, both public and private sector who are involved in the tourism industry. These annual reports are designed to provide key information to various stakeholders on tourists’ experiences in Sri Lanka, including the demographic of tourists, travel patterns and how they prefer to spend money. The data presented in these reports is based on the Airport Departure Survey and Immigration Services. These reports gave me a strong idea of which indicators are most valuable to make policy-relevant decisions in the tourism sector, including how to provide incentives to the private sector while balancing environmental considerations. At the same time, it revealed that SLTDA could further enhance its data capacity and become more equipped to gather data from different resources.

Finally, most of my weeks were spent on developing measures for how to quantify the economic contributions of tourism. Under this question, I mainly focused on employment generated by the tourism sector. While we can’t be completely certain, our preliminary work suggested that tourism-based employment directly affects 5% of total employment in Sri Lanka. In order to model how many jobs are available in the tourism sector, I relied heavily on the practices and systems used in other developing and developed countries. As I delved more into this work, again I realized that the main challenge was the scarcity of data and lack of coordination between SLTDA and other public-sector entities that can collect relevant data on behalf of SLTDA. For example, a common practice in countries with comprehensive tax record systems is to rely on administrative data to gather information on businesses that provide tourism as well as household and business surveys to measure employment. Then, further technical expertise is used to integrate these different data sources in order to arrive at a consistent measure for employment. However, in Sri Lanka, there were two main obstacles: widespread informality in the sector and the lack of a coordinated and consistent way of collecting data at both the household and establishment level. Thus, we spent time in looking at data sources from other government entities that SLTDA can rely on and how to increase coordination with such government branches. The overall aim is to build a Tourism Satellite Account, a mechanism adopted throughout the world by both developed and developing countries that provides standardized methods to measure tourism’s contributions to the national income and employment.

Once immersed in the tourism sector from a policy perspective, it is obvious how valuable it can be for a country’s social and economic development and the scale of investment required from various stakeholders in order to fulfill this potential. Furthermore, it becomes apparent that the process of designing tourism-related policies can also provide tremendous insight to other sectors and industries facing development constraints. In general terms, a sustainable tourism policy will be characterized by strong collaboration between the private and public sectors, environmental protection measures for the majority of tourism-related investments, and investment in skill development. The knowhow required for a successful tourism policy, which allows both the tourism economy and the overall economy to thrive while protecting natural assets and vulnerable households, can be a valuable tool for any country that is aiming to reap benefits from the development path that the Sri Lankan government has set for the country.

Overall, Sri Lanka’s tourism sector is moving in a positive direction. The 2020 Strategic Plan is dedicated to improve the touristic experience Sri Lanka currently has to offer- there are projects to expand the road accessibility of certain key destinations, develop accommodation options that are limited in areas that receive high numbers of tourists (for example, Anuradhapura, a UNESCO World Heritage Site but mostly offers homestay or small hotels as options for accommodation) or increase the number of trained guides offering cultural or wildlife tours. One of the main goals behind improving and facilitating how tourists experience the country is to rebrand Sri Lankan tourism and move away from the common perception that Sri Lanka is a low-cost destination for foreigners. Furthermore, the country’s recent political and economic improvements are playing a positive role in attracting donor organizations and foreign investors, introducing further growth opportunities for sectors with large contributions to the overall economy. At the same time, the main challenges faced by the Tourism Development Authority are institutional problems which do not only concern tourism. The government branches need to collaborate in a systematic manner to make use of available administrative and census data to make evidence-driven decisions. The coordination between public and private sector organizations could also be improved to design policies that will improve the quality of services offered by both parties and ensure private sector development in a sustainable manner.

Finally, in order for Sri Lankan citizens to benefit from the promising future of tourism, the government should promote employment and careers in the industry and collaborate with the private sector on workforce development by improving the policies and regulations on diversity, compensation and labor conditions. The government strategy should be to increase the attractability of tourism-based employment for underrepresented groups and maintain a motivated, engaged workforce, which in return will inevitably improve the quality of establishments providing services to tourists.

INTERVIEW: Keeping Government Priorities on Track

nment priorities as approved by the current government, under the leadership of Prime Minister Rama.

nment priorities as approved by the current government, under the leadership of Prime Minister Rama. {kind=link}

{kind=link}

Does the Sri Lankan Economy Need More University Graduates?

By Ljubica Nedelkoska, Tim O’Brien and Daniel Stock

Download PDF | Listed to the podcast interview

SUMMARY OF FINDINGS

Sri Lanka has exceptionally low rates of tertiary education admission and graduation for its level of economic development. Many have identified this as a roadblock to Sri Lanka’s economic competitiveness. Using six years of Sri Lanka’s Labor Force Survey, we study the evidence of shortages of tertiary educated workers. Our analysis casts doubt on the existence of a general shortage of university graduates in spite of the low university admission and graduation rates. We find that the majority (77%) of university graduates are employed by the public sector (government and semi-government), where they enjoy job security and other benefits but earn wages that are only a fraction of what is paid in the private sector. On average, college graduates in the private sector earn 1.6 times higher wages than college graduates in the public sector. Moreover, the wages of college graduates in the public sector are only between a quarter and a third higher than those of A-level graduates in the same sector. A minority (23%) of college graduates are employed by the private sector, where they earn significantly more than those with only A-levels – 66% in the case of men and 128% more in the case of women. These very high wage premiums in the private sector, combined with very low unemployment rates of college graduates, suggest shortages of particular types of tertiary education. This seems to be the case with ICT professionals and ICT technicians, business professionals, science and engineering professionals, and various managerial occupations. This suggests that education policy should focus on addressing the shortages in these areas, as opposed to expanding tertiary education more generally. A general expansion of higher education without a focus on these fields could actually further lower the already low returns to a tertiary degree in the public sector, without addressing any issues of Sri Lanka’s economic competitiveness.

BACKGROUND

Sri Lanka’s gross enrollment ratio (GER) in tertiary education reached close to 20% in 2015, placing it among the lowest rates of all middle-income countries. The average GER among middle-income countries is 33%, and all countries in the region, including India and Indonesia, have significantly higher tertiary education enrollment rates than Sri Lanka. This has led many to believe that Sri Lanka has too few individuals with tertiary education. In its flagship publication “Sri Lanka: State of the Economy 2017,” researchers at the Institute of Policy Studies in Sri Lanka identified skill gaps in the educational system as one of the key roadblocks towards higher competitiveness of the Sri Lankan economy. The report reads: “As of 2014, only 5 percent of 20-24-year olds were enrolled in a university, while another 8 percent were enrolled in other educational institutions and only 3 percent of the same age group were enrolled in technical education and vocational training (TVET) courses.” It goes on to explain that the main reasons for these low enrollment rates are capacity constraints of the state university system together with the low level of development of private sector education and the TVET system. In the same vein, the Government of Sri Lanka agrees that “education and skills development are currently inadequate to sustain growth through knowledge-based, competitive economic activities” and plans to increase access to secondary and tertiary education (Vision 2025).

While education serves various important roles such as intellectual enrichment, social mobility and social status, the primary purpose of education from an economic perspective is to make us more productive on the labor market. Most economists believe that the positive returns to education (i.e., the wage premium associated with an extra year of education keeping other factors constant) observed worldwide suggest that education helps companies become more productive and, in return, these companies are willing to pay higher wages for better-educated employees.

If too few university graduates is a key constraint to higher competitiveness of the economy of Sri Lanka, we would expect to see companies in the private sector fiercely competing for those few new graduates that emerge each year from Sri Lanka’s higher education institutions. As a result of this competition, we would expect the unemployment rates of university graduates to be low, and the wage premium they are paid to be high. These two characteristics would together give a clear signal that Sri Lanka is facing shortages of tertiary education graduates.

ARE SRI LANKAN UNIVERSITY GRADUATES EASILY FINDING JOBS?

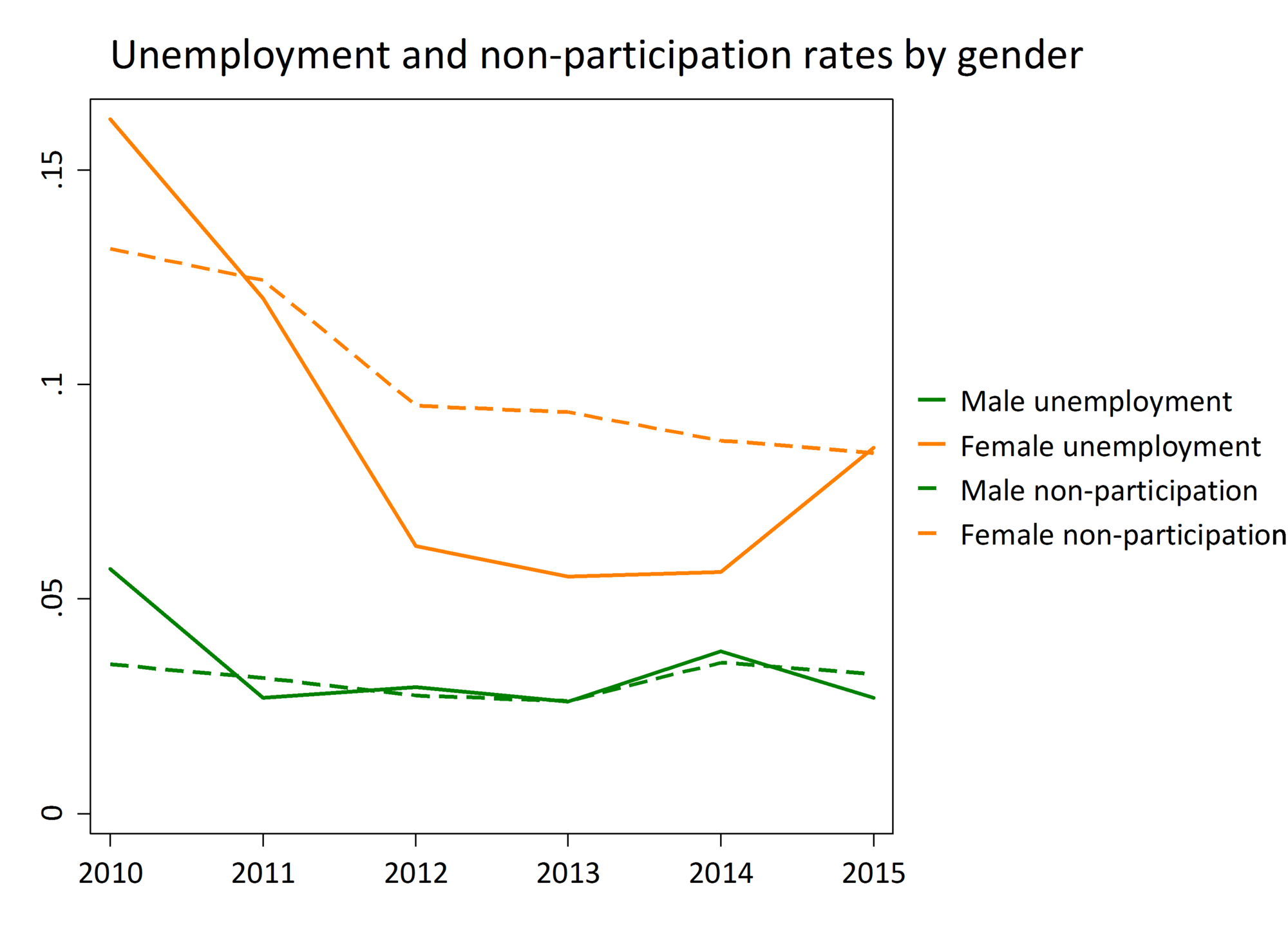

The average annual rate of net university graduates inflows into the labor market between 2011 and 2015 based on Labor Force Survey (LFS) data was around 23,000. On the aggregate, there were about as many net new jobs created for these graduates over the same time period, suggesting a very high job placement rate. As a result, the employment rates for highly educated men remained very high (about 94%), while those of highly educated women even increased, from 73% in 2010 to 84% in 2015 (Figure 1). These aggregate patterns indeed suggest that the labor market of university graduates is tight.

Figure 1: Unemployment and non-participation rates of university graduates and postgraduates by gender

Source: Labor Force Survey (LFS) Sri Lanka 2010-2015. Note: Includes 15-65 year olds, all higher education levels and institutions.

DO UNIVERSITY GRADUATES RECEIVE HIGH WAGE PREMIUMS AT THE JOB?

As a reference, a college graduate in OECD countries, where the supply of tertiary educated is significantly higher than in Sri Lanka, earns about 57% more than a counterpart with no more than a high school education. The United States has earnings premium on the high end at 77%. In Sri Lanka, across all sectors, the premium to tertiary education over A-levels was 51% in 2015 (Figure 2), which is decent, but below the OECD average. Given the low supply and high rate of employment of university graduates, one would expect to see higher wage premiums. This leaves us somewhat puzzled: why should a country with drastically lower supply of university graduates than OECD countries have lower than average returns to tertiary education? Such pattern could indicate that the education obtained through the university system is not particularly valuable to the employers. The average premium could also disguise important differences in the returns to a tertiary degree among different groups of graduates. We think that the group distinction that will help us best explain the above patterns is the one between university graduates who opt to work in the public sector and those who opt to work in the private sector.

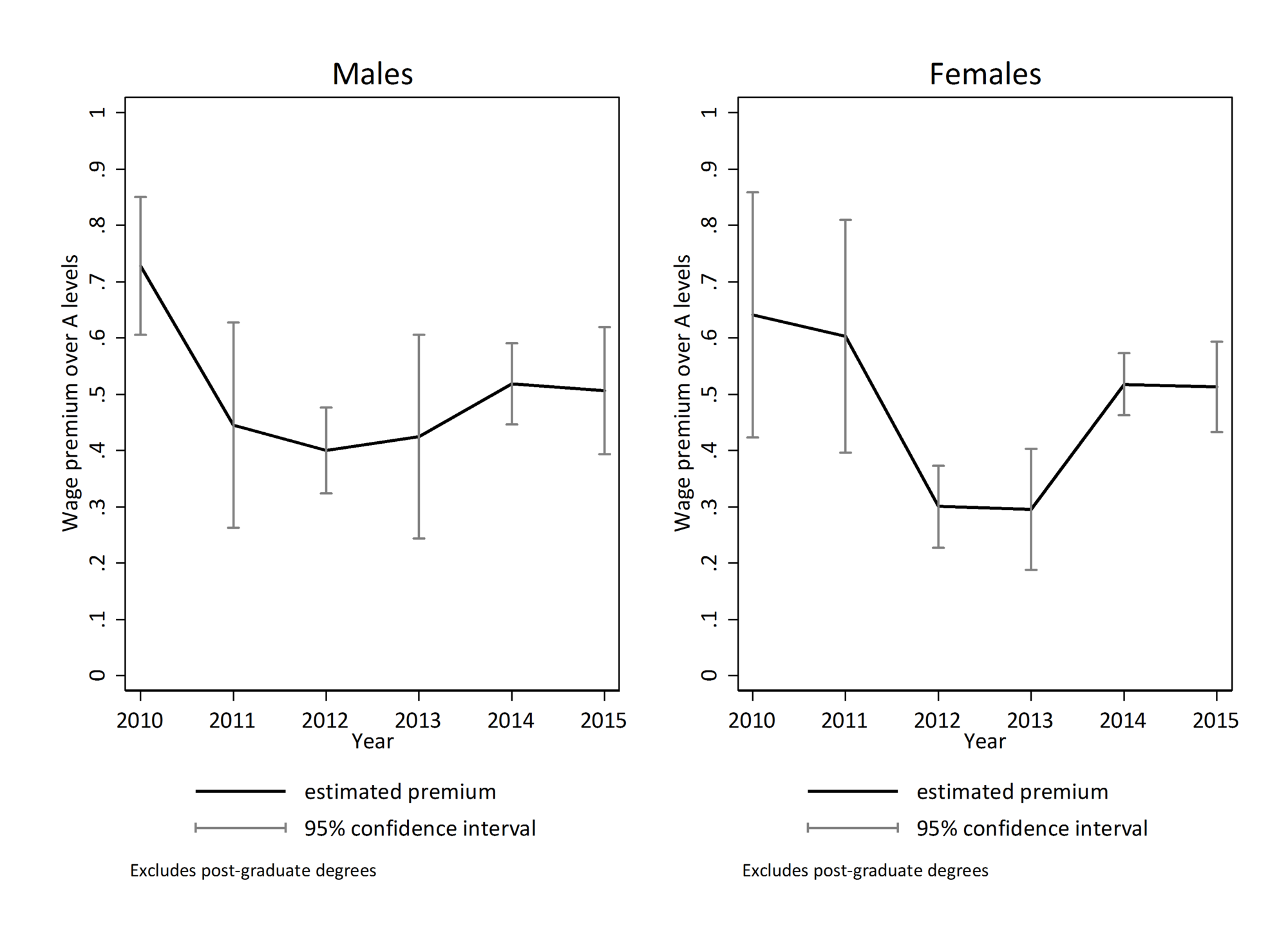

Figure 2: Premium of a college degree over A-levels

Source: Labor Force Survey (LFS) Sri Lanka 2010-2015

Note: Includes 15-65 year olds. To keep the group of college graduates homogenous, the premium is estimated for those with Bachelor’s degrees only, i.e., we exclude those with post-graduate degrees. Each estimate is the coefficient of a dummy variable indicating whether a person completed a Bachelor’s degree from a Mincer regression that controls for potential work experience and labor market entry cohort effects. Separate regressions were run for each year and gender combination. The reference educational category is those with completed A levels. The dependent variable is the log of the real hourly wage.

In 2015, the private sector only employed 23% of all university graduates, while the government and the semi-government sector employed the other 77%. This casts a doubt on the claim that the private sector is hungry for university graduates in general. The patterns of premiums to a college degree by sector introduce another layer of complexity to the story. The premium is low in the public sector, where college-educated men earned a 36% premium over A-levels and college-educated women earned a 25% premium over A-levels in 2015. Whereas in the private sector, college-educated men earned a 66% premium over A-levels and college-educated women earned a whopping 128% premium (Figure 3). A further comparison of the university graduates in the public versus the private sector shows that a male university graduate, on average, earned 1.5 times more per month in the private sector than in the public sector, while a female university graduate, on average, earned 1.7 times more.

Figure 3: Premiums to tertiary education by sector and gender

Source: Labor Force Survey (LFS) Sri Lanka 2010-2015.

Note: Includes 15-65 year olds. To keep the group of college graduates homogenous, the premium is estimated for those with Bachelor’s degrees only, i.e., we exclude those with post-graduate degrees. Each estimate is the coefficient of a dummy variable indicating whether a person completed college education from a Mincer regression that controls for potential work experience and labor market entry cohort effects. Separate regressions were run for each year, sector and gender combination. The reference educational category is those with completed A levels. The dependent variable is the log of the real hourly wage.

WHY IS THE PRIVATE SECTOR EMPLYING FEW UNIVERSITY GRADUATES BUT PAYING SIGNIFICANT PREMIUMS, WHILE THE PUBLIC SECTOR IS EMPLOYING MANY BUT PAYING LOW PREMIUMS?

Why don’t more university graduates go to the private sector where wages are high, and capture some of these earnings differences? There can be different reasons for this, but here we will focus on one very important reason. The types of university graduates that the private sector needs are quite specific. They are different from those employed by the public sector and different from the majority of graduates produced by the university system. The most common professions for university graduates in the private sector are: managers and production managers (25%), science and engineering professionals (14%), business administration associate professionals (10%), teaching professionals (9%), business and administration professionals (6%), ICT professionals (5%) and science and engineering technicians (5%). The most common professions for university graduates in the public sector are: teaching professionals (45%), business administration associate professionals (18%), clerks (8%), and health professionals (8%) (Figure 4).

Figure 4: Occupational composition of university graduates by sector

Source: Labor Force Survey (LFS) Sri Lanka 2010-2015.

Note: Includes 15-65 year olds. The estimated shares are averages over 6 years. Sorted by share of employees in the private sector. Includes the 17 (out of 38) largest occupations in the private sector. All excluded occupations contribute less than 1% of employment in both the private and the public sector.

WHICH PROFESSIONS ARE MOST LIKELY IN SHORT SUPPLY?

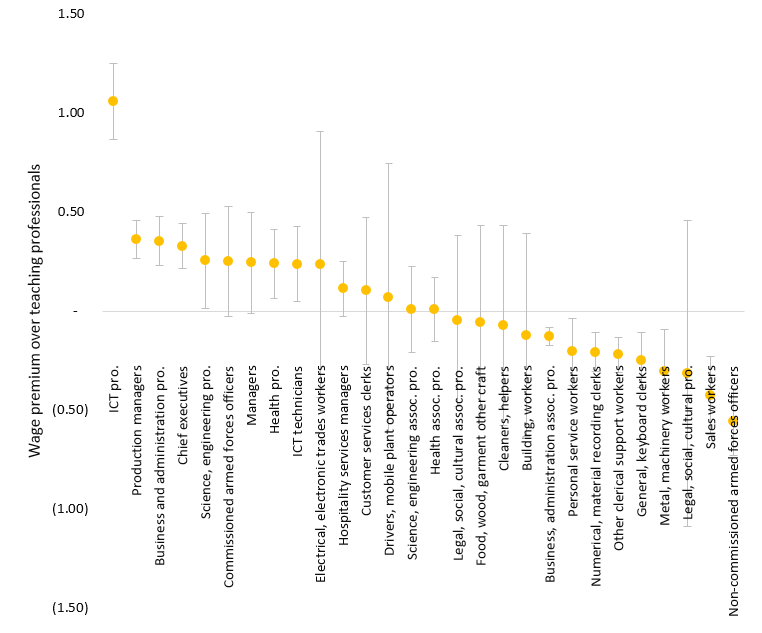

We compare the hourly wages of university graduates in various occupations, regardless of whether public or private sector, to the hourly wages of the teaching professionals (the largest group among university graduates). We control for the level of labor market experience, gender, cohort effects, and for whether one has a post-graduate degree, to ensure that we compare the wages of individuals that are otherwise similar. ICT professionals earn 106% more than teaching professionals; production managers and chief executives earn 33-35% more; engineers earn 25% more; and health professionals and ICT technicians earn 24% more than teaching professionals (Figure 5). Having a post-graduate degree is associated with additional 20% premium. As anticipated, most of the professions with higher returns than the teaching profession are typically employed in the private sector. By paying wages significantly higher than the ones of the typical employee with tertiary education, the private sector is signaling that they need these specific professions and that they may have hard time finding such candidates in the Sri Lankan labor market. In other words, these are the professions/educational fields where an expansion of the tertiary education could most likely help relax a skill shortage constraint. Outside these professions, we find little evidence of educational shortages at the tertiary level.

Figure 5: Occupational premiums among university graduates

Source: Labor Force Survey (LFS) Sri Lanka 2010-2015.

Note: Includes 15-65 year olds, all sectors, tertiary graduates only. Results from a Mincer-like equation, but with occupational dummies instead of education. Controls include potential labor market experience and its square term, labor market cohort dummies, a gender dummy and a dummy for having a post-graduate degree. The whiskers correspond to the 95% confidence intervals. The dependent variable is the log of the real hourly wage.

CONCLUSIONS AND POLICY DISCUSSION

Using data from the Labor Force Survey of Sri Lanka (2010-2015), we study the claim that skill gaps resulting from the restrictive tertiary education system of Sri Lanka present a serious challenge to the economic competitiveness of Sri Lanka. Theoretically, skill gaps can restrain companies’ choice of employees, both in terms of numbers and quality. There are two straightforward tests that we perform in order to see whether such skill gaps exist. First, we check if college graduates have an easy time finding jobs in Sri Lanka, and second, we measure the returns to their college degrees. We expect that employment rates are high and returns to education are high for degrees that are in short supply. We find that this is the case only with a subset of occupations/educational fields at the university level: ICT professionals and technicians, managers and executives, business and administration professionals, science and engineering professionals, and health professionals. The majority of these are employed in the private sector where, the returns to a college degree are high. However, the private sector only employs 23% of all university graduates, while the public sector (government and semi-government) employ the other 77%. The public sector pays 40% less than the private sector wages paid to university graduates on average. Unless the public sector vastly compensates for this wage differential with more generous fringe benefits and higher job security, we have to conclude that we only find evidence for skill gaps in a fraction of Sri Lanka’s college majors listed above.

The Vision 2025 of the Government of Sri Lanka (GoSL) envisages an expansion of the tertiary education system. Our findings inform that, when doing so, GoSL should focus on the expansion of particular college majors, and not on the general expansion of the higher education system. Increasing the access to ICT, managerial, engineering, business and healthcare professions in particular would benefit the Sri Lankan economy as it will expand the companies’ choice of workers and enable them to grow faster that they can do now.

A question to explore further is whether the scope of this expansion should go beyond the system of higher education, and include the system of vocational training and secondary education. Previous research (Dundar et al. 2017) has shown that the capacity of science and engineering education at the tertiary level is restricted by the low capacity of the secondary education to equip the students with the basics of science, meaning that the expansion of tertiary education in these fields will need to be accompanied by expansion of science education at the secondary level. Moreover, Sri Lanka has a well-developed system of vocational training and it is worthwhile exploring whether the TVET could partially help bridge some of these gaps with strong participation of the private sector that is facing the skill shortages.

Finally, like most developing economies, Sri Lanka faces significant brain drain. Sri Lanka is a net exporter of many professions including engineers and engineering technicians (Growth Lab at CID 2018). Although Sri Lanka pays high wages for engineers relative to other professions in the country, Sri Lanka does not pay internationally competitive wages for their professionals. The salary of a mid-level engineer in Colombo for instance was among the lowest in Asia and Oceania in 2012 (JETRO 2013) – about half of what a mid-level engineer is paid in Beijing and only 16% of what the equivalent engineer is paid in Singapore. However, Sri Lanka does not have a choice but to further expand the supply of shortage professions. Only a supply push can help the existing industry expand and potentially attract further capital investments, including foreign investments in Sri Lanka.