Student Stories: Forecasting Inflation for the UAE

Fernando Mundaca is currently pursuing a master’s degree in the MPA/ID program at Harvard Kennedy School (expected graduation in May 2023). He was accepted into the Growth Lab’s 2022 Summer Internship Program and contributed to the UAE project. Our team is developing rigorous research to inform the Ministry of Economy in devising a dynamic trade policy, geared towards promoting structural transformation in the UAE and achieving sustained long-term economic growth.

Why did you apply to be a Growth Lab intern?

I found the project on diversification of the UAE’s economy very interesting. I wanted to work in a country set-up that was completely different to what I was used to (South American government).

What did you work on this summer?

I worked on a model to forecast/nowcast inflation in the UAE. Because of the international context, high inflation in the country was a concern for the Ministry of Economy. I divided the CPI into four components and worked a model for each component.

In what ways were you challenged?

Working in a new country for a new institution, locating and accessing information was a challenge. The ministry is a large and complex organization that I had to quickly learn how to navigate if the project was to be successful.

What was your most exciting experience?

Getting to know a different government type (monarchy) and monetary policy (exchange rate pegged to the dollar) were the most exciting aspects of doing the internship.

What advice would you give future Growth Lab interns?

I would advise them to have patience even if the internship seems short. There is enough time to do something productive and interesting.

What’s next for you?

After the program, I am going back to the Central Reserve Bank of Peru to try to apply some of the tools learned at HKS.

Student Stories: Developing Diversification Strategies for African Countries

Benedikt Margraf is a second-year MPA student at the London School of Economics and Political Science. As part of the Growth Lab’s 2022 Summer Internship Program, he contributed to the newly formed Pan-Africa research agenda. Our team is exploring the Africa Continental Free Trade Area (AfCFTA) and the underlying constraints that have held African nations back from economic diversification and structural transformation.

Why did you apply to be a Growth Lab intern?

The Growth Lab constituted an excellent opportunity to deepen my interest in economic growth constraints with an empirical-analytical focus.

What did you work on this summer?

My work focused on the development of national export diversification strategies in the context of the African Continental Free Trade Area Agreement.

In what ways were you challenged?

Although AfCFTA has already been ratified and is in force, implementation is still very much in its infancy. Identifying concrete export opportunities and existing constraints therefore requires very detailed research at the product and industry level, extensive econometric analysis and background discussions with institutional stakeholders. Exciting and challenging at the same time.

What was your most exciting experience?

I especially enjoyed the inspiring colleagues and teamwork.

What advice would you give future Growth Lab interns?

Be curious and apply!

What’s next for you?

I will start the second year of the two-year MPA program, specializing in Economic Policy.

Student Stories: From DEV 309 to Analyzing WAEMU’s Impact on Trade

Julia Conrad is a second-year MPA/ID student at Harvard Kennedy School. She was accepted into the Growth Lab’s 2022 Summer Internship Program and contributed to the newly formed Pan-Africa research agenda. Our team is exploring the Africa Continental Free Trade Area (AfCFTA) and the underlying constraints that have held African nations back from economic diversification and structural transformation.

Why did you apply to be a Growth Lab intern?

In Fall 2021, I completed the Development Policy Strategy (DEV-309) course with Professor Ricardo Hausmann. It was a great learning experience and one that I hoped to build on with this opportunity. As the regional focus of the internship was Africa, it was especially interesting and fitting to my background and experience.

What did you work on this summer?

For the case of the West African Economic and Monetary Union (WAEMU), I analyzed how the establishment of a regional economic bloc has translated into increased trade and investment among member countries and within the region. [Read Julia’s blog on this research]

In what ways were you challenged?

I initially intended to talk to policymakers and trade practitioners in WAEMU to discuss the Growth Lab’s research agenda on AfCFTA and to receive feedback on some tools that were developed. Unfortunately, the outreach via Zoom/email was more difficult than expected, also given that my internship fell into the holiday season of many institutions and ministries.

What was your most exciting experience?

I very much enjoyed the Growth Lab’s Development Talk seminar with economist and Namibian Finance Minister Iipumbu Wendelinus Shiimi.

What advice would you give future Growth Lab interns?

I believe it could be more fruitful to work on a research question as a team of interns or to be paired with a full-time Growth Lab research staff. Therefore, I recommend future interns consider aligning in advance.

What’s next for you?

I am leaving for a trekking trip to the Peruvian Andes and after I will attempt to climb Cotopaxi in Ecuador (wish me good luck!).

Student Stories: Unlocking Green Hydrogen in Namibia

Henry Rounds is a second-year MPA/ID student at Harvard Kennedy School. He was accepted into the Growth Lab’s 2022 Summer Internship Program and contributed to the project in Namibia. This two-year policy engagement with the Government of Namibia focuses on supporting implementation efforts on a range of growth- and inclusion-related challenges.

Why did you apply to be a Growth Lab intern?

As a result of my growing interest in understanding the levers of economic growth and equitable distribution, I applied to the Growth Lab Namibia project to work directly with the government on a project aimed at harnessing the resources of the private sector to spur new growth and create jobs.

What did you work on this summer?

Over the summer, I was tasked with identifying how Namibia could unlock future growth as it invests in developing a green hydrogen industry. In particular, I focused on understanding the kinds of industries that could thrive in a cheap green energy context and the skills the Namibian workforce will have to develop to benefit fully.

“What’s exciting is simply Namibia’s opportunity to develop a brand new industry that will be in high demand in the future and one that it is competitively positioned to produce, given its geography.”

Henry Rounds MPA/ID 2023

In what ways were you challenged?

One of the most challenging aspects of the work was the multiplicity of stakeholders involved, each with their own priorities. Moving forward means getting everyone on the same page, a challenging task across government agencies, not to mention private actors.

What was your most exciting experience?

What’s exciting is simply Namibia’s opportunity to develop a brand new industry that will be in high demand in the future and one that it is competitively positioned to produce, given its geography.

What advice would you give future Growth Lab interns?

Define your scope early and talk to as many folks as possible, no matter what their role. Also, travel as much as you can to get to know the country and work with other interns if possible!

What’s next for you?

I’m looking forward to continuing my work on Namibia as part of my SYPA, and deepening my ability to apply Growth Lab’s approach to the questions that arose this summer.

Student Stories: Fighting Altitude and Teaching Public Policy in Bolivia

Marco Brancher is a second-year MPA/ID student at Harvard Kennedy School. He was accepted into the Growth Lab’s 2022 Summer Internship Program and participated in our engagement with the Master’s Programs for Development (MpD) at Catholic University of Bolivia. This focus of the project is to strengthen the teaching and studies of the public policy challenges in Bolivia.

Why did you apply to be a Growth Lab intern?

I applied to the Growth Lab because I was eager to learn more about Economic Complexity and I wanted to have the teaching experience.

What did you work on this summer?

During the summer I taught a few classes in Bolivia, exploring my experience with data analysis for public policies and microeconomic theory. Moreover, I am writing a report using a gravity model with complexity components to better assess the products the country should be exporting to develop its economy.

In what ways were you challenged?

I was challenged in every way. First, I was challenged by the altitude of La Paz and by the pressure of teaching classes in Spanish in a hybrid environment. Then I was challenged by the data gathering process and by the econometric estimation. Finally, I think it was super hard to really understand the Bolivian economic constraints.

What was your most exciting experience?

Certainly, teaching! It was an incredible experience to be able to prepare the classes and receive the students’ feedback. After this experience, I realized that I could learn a lot by teaching and interacting with students.

What advice would you give future Growth Lab interns?

Try to spend the most time possible in the country where you are going to work!

What’s next for you?

I’m not sure! I’ll probably continue to work with macro policy and development issues, focusing on structural change and inequalities.

Student Stories: Overcoming Unique Challenges in the UAE

Harumi Hasegawa Sanchez is a second-year MPA/ID student at Harvard Kennedy School. She was accepted into the Growth Lab’s 2022 Summer Internship Program and contributed to the UAE project. Our team is developing rigorous research to inform the Ministry of Economy in devising a dynamic trade policy, geared towards promoting structural transformation in the UAE and achieving sustained long-term economic growth.

Why did you apply to be a Growth Lab intern?

I found this opportunity unique for having such a dynamic balance between research and applied work to real-life situations where I can put into practice my academic and professional experience.

What did you work on this summer?

I collaborated closely with the UAE’s Ministry of Economy working on micro- and macroeconomic main policy reform topics. Specifically, I studied the economic history of the UAE to understand the main drivers of the diversification process since the establishment of the country. Also, I developed GDP nowcasting models to strengthen the Ministry’s forecasting methods.

In what ways were you challenged?

The UAE is a completely different country in terms of how the economy works, the political dynamics, its society and public policy targets. These differences challenged my previous knowledge and preconceptions about how a country should or usually works and what they should look for. I learned a lot in this process, and it opened my mind to different realities.

What was your most exciting experience?

When the Growth Lab team came to the UAE, the interns participated in meetings with different authorities in Dubai and Abu Dhabi; including the Ministry of Industry, the Department of Economic Development, and leaders in trade negotiation and research departments, among others. This was key to deepening my understanding of the country.

“Make the most of the internship experience by choosing a combination of a country that you know less about and the topic that you are most interested in.”

Harumi Hasegawa Sanchez MPA/ID 2023

What advice would you give future Growth Lab interns?

Take the opportunity to broaden your knowledge and make the most of the internship experience by choosing a combination of a country that you know less about and the topic that you are most interested in. In this way, you get to apply some of the tools that you know in a totally different environment.

What’s next for you?

In the short term, preparing for my second and last year of the MPA/ID where I want to keep challenging myself on learning new topics such as political economy and macroeconomic crisis, as well as looking forward to honing my skills in leadership and negotiation.

Student Stories: Exploring Investment Opportunities in Namibia

Caitlin McIlwain is pursuing her MPA at the London School of Economics and Political Science. She held an internship with the Namibia Investment Promotion Development Board and contributed to the Growth Lab’s project in Namibia. This two-year policy engagement with the Government of Namibia focuses on supporting implementation efforts on a range of growth- and inclusion-related challenges.

Why did you apply to be a Growth Lab intern?

Miguel Santos! Just kidding. I really like the Growth Lab’s philosophy that a way to measure growth is through complexity. Their tools just make sense to even the average person, and often when making policy, that’s the person you need to pander to. I wanted experience in the development sector and I had never travelled to Africa. I spent a lot of time researching Namibia before I applied and found its history fascinating and complex. I was up for the challenge.

What did you work on this summer?

I worked for the Namibia Investment Promotion Development Board which is a public organization under the office of the president in Namibia. I worked with the investment and new ventures team to drive investments to the appropriate industry sector (the sector that was most feasible and attractive for Namibia to grow into) and to facilitate efficiency gains among private and public sector participants who experienced significant constraints to growth.

“Having never been to Africa before and being the only (and first) intern in the NIPDB office, it was challenging to find my footing at first. I had to become independent and self-sufficient quickly…”

Caitlin McIlwain LSE MPA 2023

In what ways were you challenged?

Having never been to Africa before and being the only (and first) intern in the NIPDB office, it was challenging to find my footing at first. I had to become independent and self-sufficient quickly, working on research projects and tasks that were really different from what I’d done in my working life before. I was also having discussions about Namibia’s future with Namibians who had been invested in development long before I arrived, so it felt that I had some catching up to do to be able to participate to the fullest extent.

What was your most exciting experience?

Towards the end of my internship, I worked on a slide deck detailing the ins and outs of green hydrogen for a layman’s understanding, noting that I had very little scientific background going into it. I spent days researching green hydrogen and how it could benefit Namibia and I’m surprised by how much I was able to learn and synthesize for a more basic audience’s understanding. I actually became really passionate about green hydrogen. Non-work related: a leopard walking along the road next to our car when on safari in Namibian’s biggest national park, Etosha.

What advice would you give future Growth Lab interns?

Explore the Atlas tool in detail and learn as much as you can about your specific country’s history, politics, demographics, and even geography. Everything is important and will likely be relevant in your internship. I know more about Namibia than I do about England at this stage.

What’s next for you?

Honestly, I’m not sure. I have a whole year to figure out which path of policy I want to go down. Something related to development policy healthcare policy would be ideal.

What we learn from WAEMU for regional integration on the African continent

By Julia Conrad

Created in 1994, the West African Economic and Monetary Union (WAEMU) was established as a trade and currency union and encompasses the eight countries Benin, Burkina Faso, Côte d’Ivoire, Guinea-Bissau, Mali, Niger, Senegal, and Togo1– all of which are equal members of the regional and economic union ECOWAS, the Economic Community of West African States.2 The adoption of a common currency among states is regarded as one of the highest forms of economic integration.3 Literature suggests that the establishment of a monetary union leads to increased economic activity through a rise in trade or investment flows between member countries and higher macro-economic stability.4,5, 6

WAEMU as an economic union emerged from colonial arrangements. Critics also describe it as “colonial relic” that is meant to preserve the dominance of Paris and French companies in West Africa.7 It was initially aimed at reducing transaction costs, facilitating the free movement of persons, goods, services, and capital among its members.8 The IMF and some global bodies have consistently described WAEMU as successful regional bloc with a high level of economic integration.9,10 Our analysis at the Growth Lab has found little evidence for this assessment. In contrast, it seems that many critics are right in pointing towards worrying low levels of trade and investment across the bloc. They claim that low inflation can be regarded as WAEMU’s single achievement, and even then, the question remains whether anti-inflationary governance is appropriate in the development context of Africa.11

Four working principles are at the core of WAEMU: (1) a peg of its exchange rate to the French currency, (2) free income and capital transfers within the zone and with France, (3) the French treasury promises to lend euros to the Central Bank of West African States bank (BCEAO) if they exhaust own foreign exchange reserves (this “convertibility guarantee”), and in return (4) the BCEAO must deposit at least 50% of its foreign currency reserves in a special ‘operations account’ of the French treasury – a condition that was finally lifted in 2019.12

All Euro-XOF (CFA franc) conversions used to pass through this operations account. When it was in credit, the French treasury paid interest and when it was in debit, the guarantee was active – a scenario that only happened back between 1980-1993. A French representative also used to sit on the board of the BCEAO, but this was recently also changed.13,14 The experience of WAEMU has even animated ECOWAS leaders to envisage the implementation of the currency “Eco” across the whole of West Africa, but its launch has been repeatedly postponed, last in 2020.15 A Pan-African monetary union was also part of earlier AfFCTA discussions. Its vision was partly realized under the introduction of a Pan-African Payments and Settlement System (PAPSS) in early 2022.16

“CFA franc” is essentially the name of the only two currency unions on the African continent under the West African CFA franc (XOF) and the Central African franc (XAF). Although separate, the two currencies have always been at parity and are effectively interchangeable.17 Our analysis focused on the West African CFA franc to understand what the integration under one monetary system has meant for its members’ economic stability and regional economic activity. A special focus was on the question of whether integration has led to the promise of increased levels of regional trade or investment, similar to what has been observed among member countries after the establishment of the EU.18 We also looked at how WAEMU compares in these areas with other regional economic communities (RECs) on the continent.

ON WAEMU

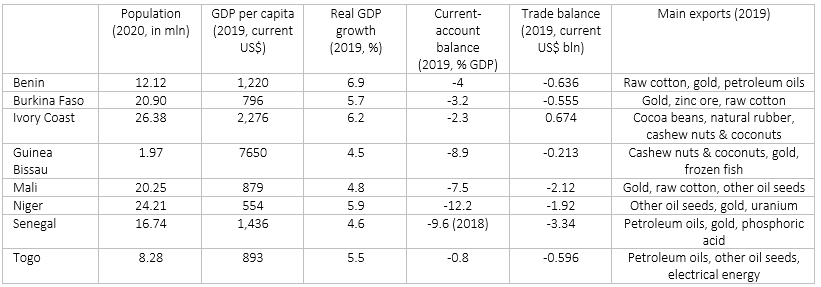

WAEMU consists of eight relatively small states with similar market structures of which all but Guinea Bissau (Portuguese) share French as an official language.19 Some annual economic statistics of WAEMU’s member countries (before Covid-19) are summarized in the table below.

Table 1: Overview of WAEMU member countries

Source: World Bank Database, Atlas of Economic Complexity

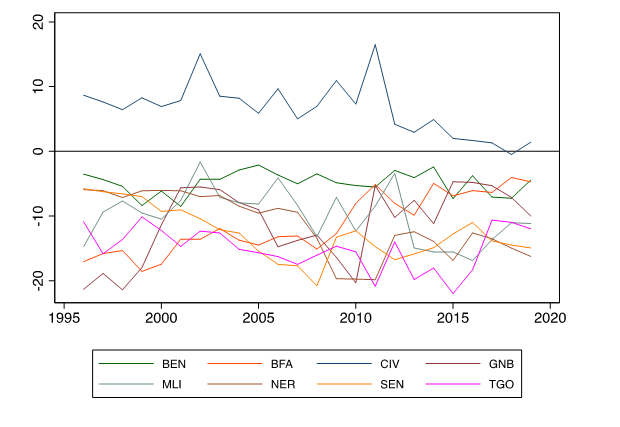

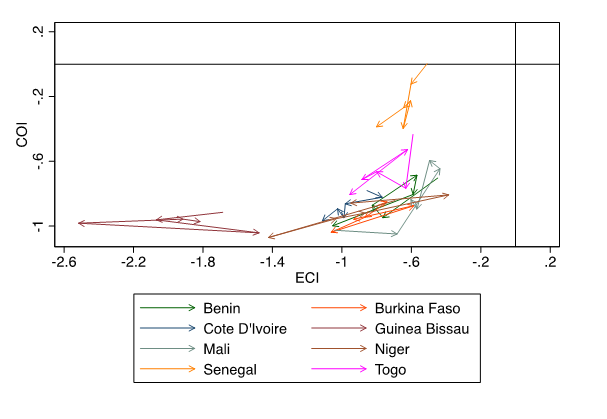

Apart from Ivory Coast, member states’ trade balance over the past 20 years has been consistently negative (see Graph 1). WAEMU states also perform relatively poor on Economic Complexity measures, as captured by the Economic Complexity Index (ECI) and Complexity Outlook Index (COI) in Graph 2. The ECI summarizes a country’s capabilities as regards production possibilities while the COI reflects the availability of good diversification opportunities for its export basket. The graph shows that WAEMU states have remained within the negative ECI and COI zone indicating little space to improve and few opportunities for economic diversification. For most WAEMU countries, the arrows also direct to the lower left of the graph, meaning that countries have become even less complex between 2015-19.

Graph 1: Trade balance of WAEMU countries from 1996-2019

Graph 2: ECI and COI evolution of WAEMU countries between 2015-2019

COMPARISON WITH OTHER RECS

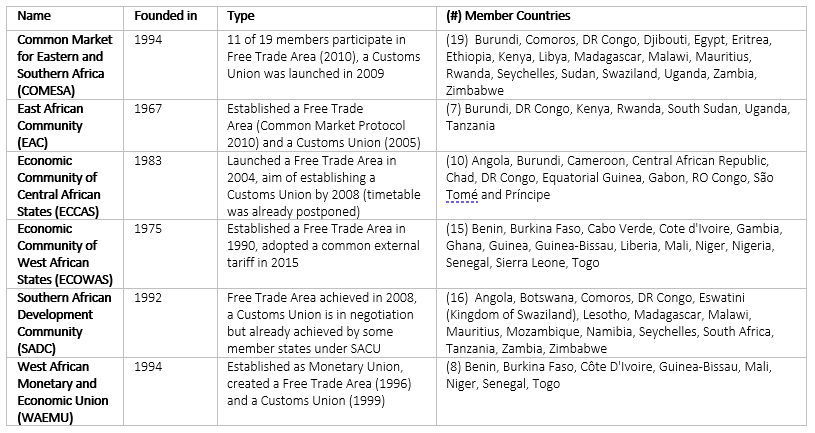

We compared WAEMU’s export structure with other RECs on the continent to see if there was any visible impact of sharing the CFA franc as currency on trade. The following table gives an overview of the selected RECs.

Table 2: Overview of RECs included in the Analysis

Note: RECs in Africa that are not included are The Community of Sahel–Saharan States (CEN-SAD), The Intergovernmental Authority on Development (IGAD), The Arab Maghreb Union (AMU) and The Southern African Customs Union (SACU). All information is based on own desk research.

As regards the economic development level, SADC, COMESA and ECCAS show a higher average income level, reaching a GDP per capita (current $) of over $2,500 GDP in 2019.20 For ECOWAS, WAEMU and EAC it was below $1,500. Unemployment has been especially high among SADC states (above 10% on average since 1999) while it was lowest (below 5%) in EAC and WAEMU. Average Inflation in WAEMU has been relatively low and remained below 5% since 2010. Since 2010 external debt in all RECs has been rising. The government’s debt burden was highest in COMESA, ECOWAS and EAC in 2019, with average debt levels of above 50%.

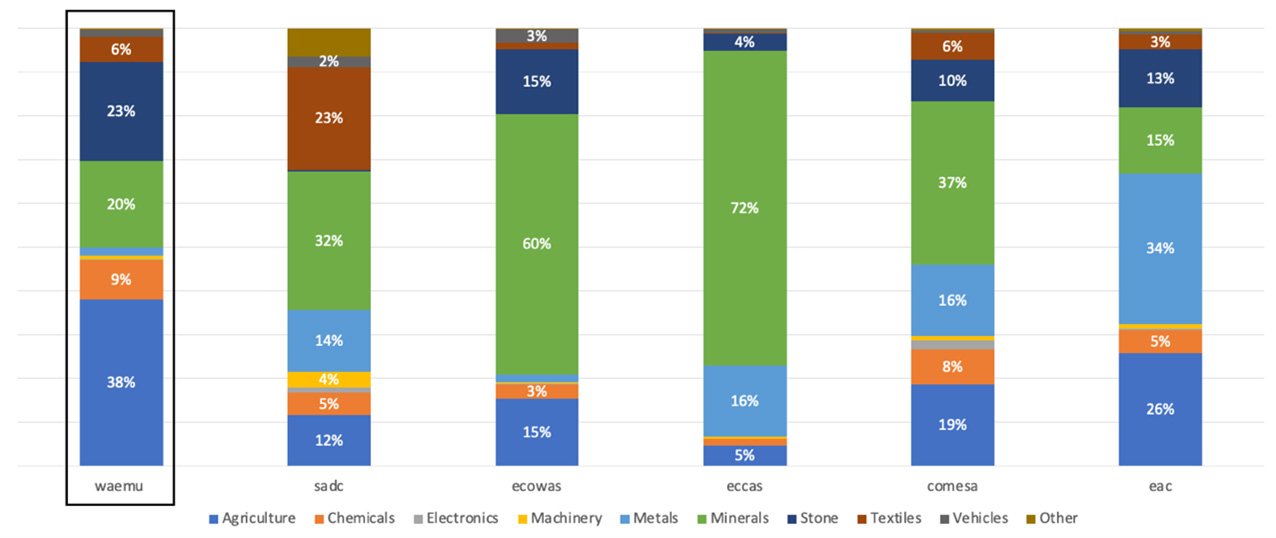

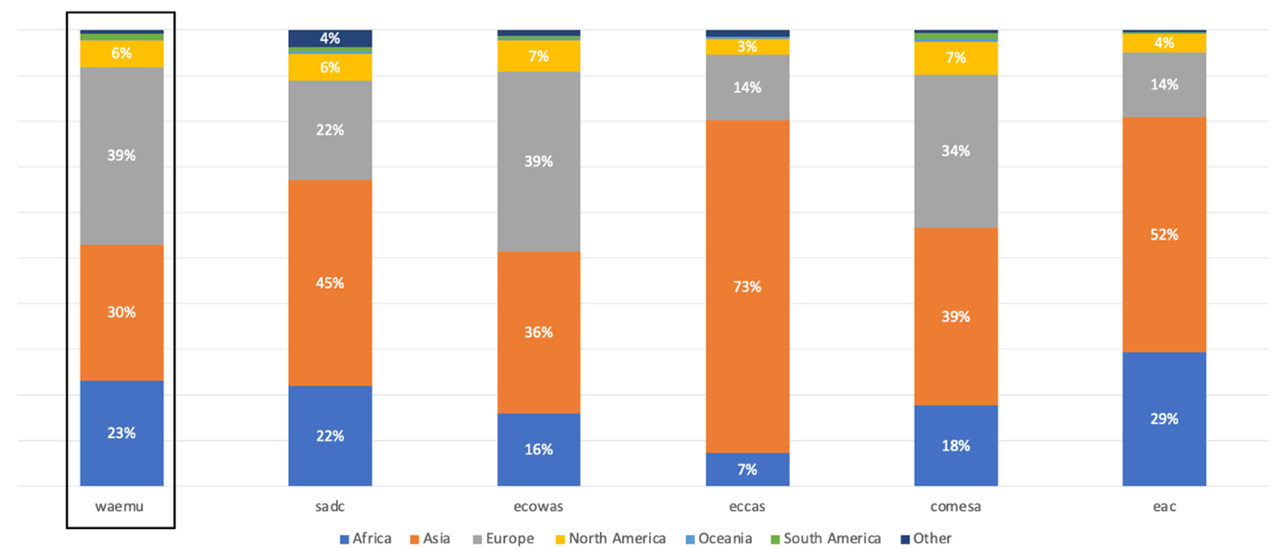

The composition of export baskets varies but it is in all RECs dominated by minerals, non-transformable commodities, and agricultural products, which are not integrated in regional supply chains and are hence shipped abroad (see Graphs 3 & 4). Exports in ECOWAS and ECCAS have mainly (>=60%) consisted of minerals. Minerals export in SADC and COMESA has been less significant but was still high (~1/3). In WAEMU, agricultural products (cocoa, raw cotton, cashew, and cocoa nuts) dominate the export basket, followed by stones (primarily gold). Interestingly, WAEMU also has the highest share of chemical products that is exported (Senegal, for example, exports 8% of the world’s phosphoric acids used in fertilizers21 ). With $9.6 billion in total export value in WAEMU and $38.5 billion in ECOWAS, Europe remains the primary trade destination in West Africa, accounting for 39% of all exports in both RECs. For East and South African blocs, Asia has overtaken Europe as the primary export destination. In ECCAS, Asia makes up as much as 77% of all exports. With 29% the EAC has had the highest share of exports within the African continent.

Graph 3: What did RECS export in 2019?

Graph 4: Where did RECS export to in 2019?

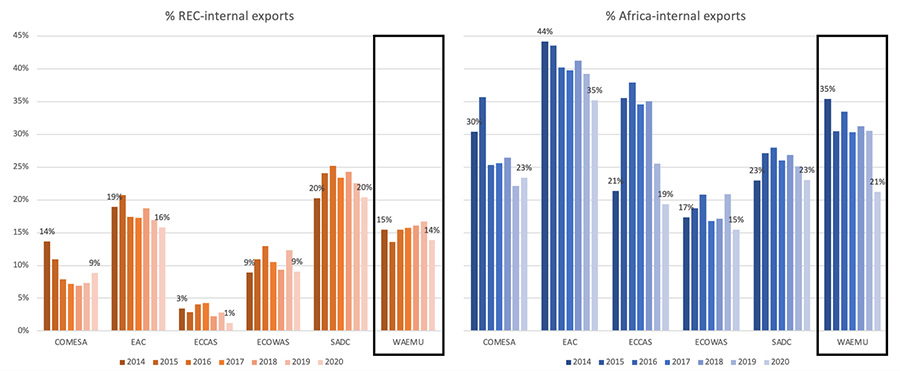

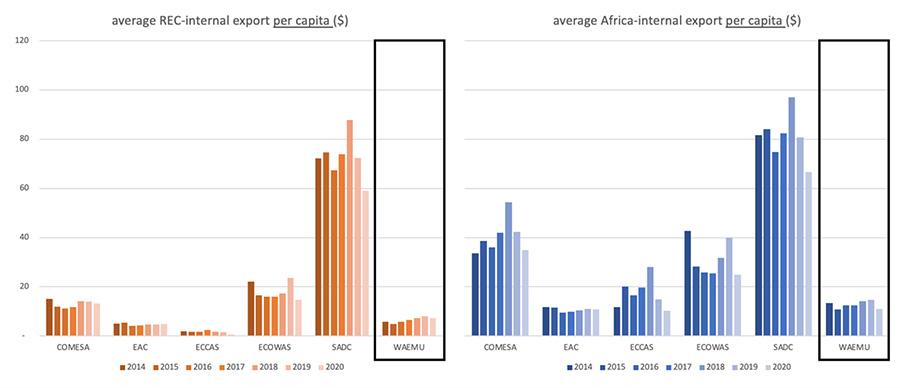

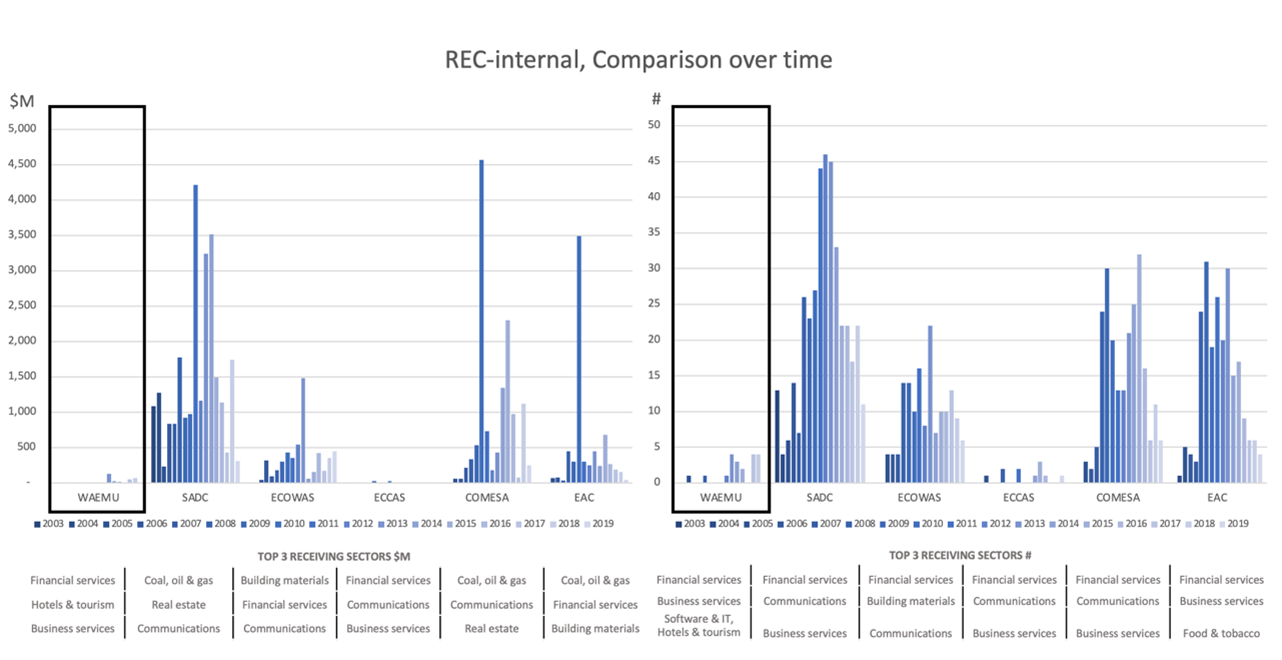

Graph 5 compares the share of regional, which means REC-internal and Africa-internal, exports for the period 2014 to 2020. Community-internal export was highest among SADC and EAC countries, with 20% and 16% of internal exports in 2020 respectively. Despite the promise of facilitated trade through a common currency, WAEMU’s internal trade business did not stand out, neither REC-internally nor for exports to the continent, and it was mainly reliant on refined oil. It was equally low in per capita terms, in contrast to SADC for example.

Graph 5: Regional exports 2014-2020

Graph 6: Regional FDI flows 2003-2019

Note: Calculations are based on investment deal announcements as captured by fDi Markets.

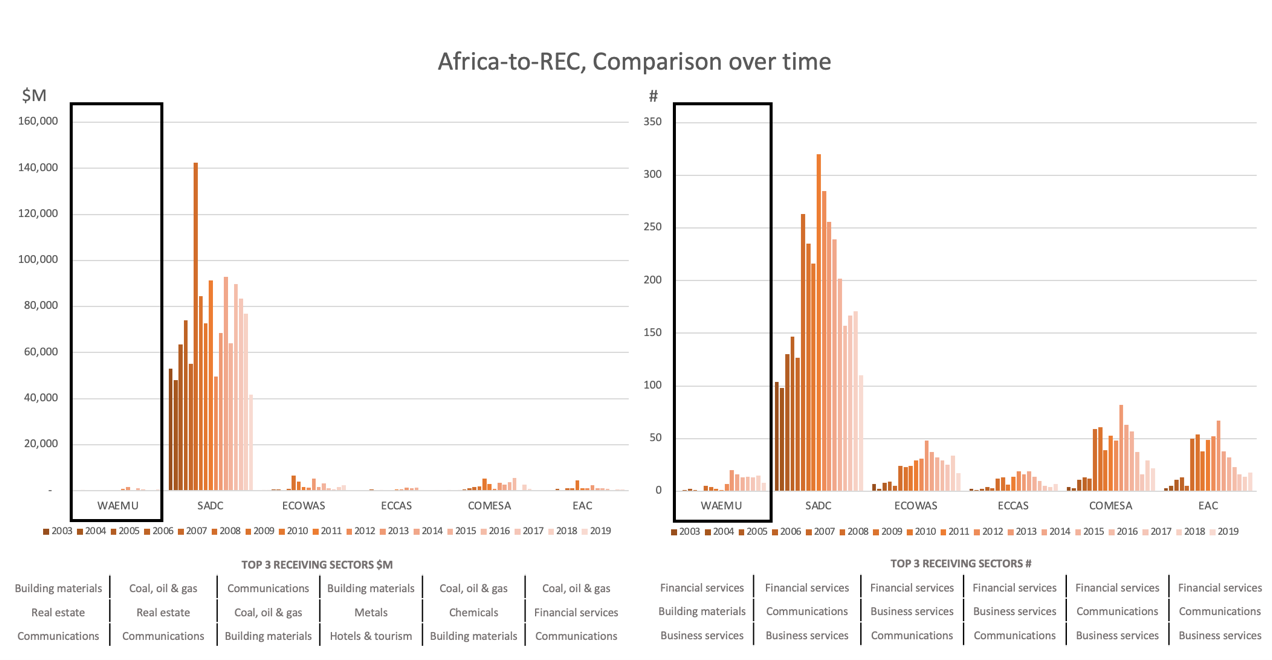

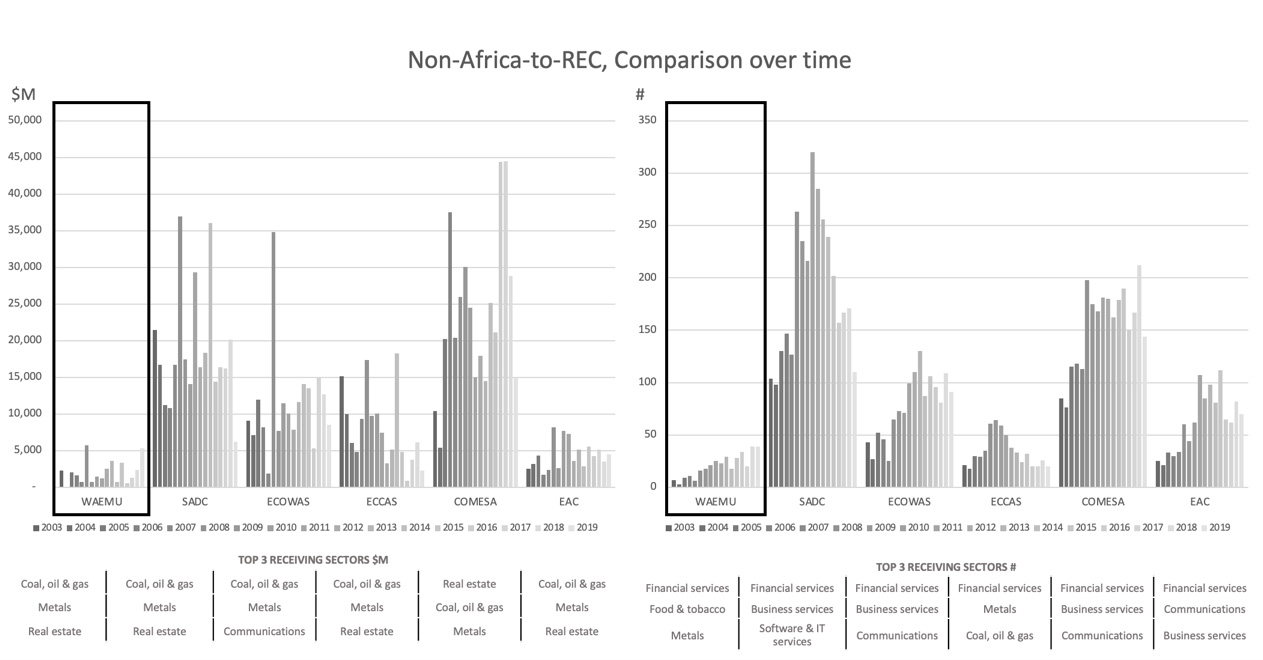

WAEMU has similarly not attracted more bloc-internal investment (Graph 6). Between 2003-2019, the group’s internally announced deals were only a small fraction (<10%) of the deals within EAC, which is a grouping of a similar size. REC-internal announcements were most frequent in SADC where almost 400 projects of more than $25 billion were planned. WAEMU lags similarly behind in generating investments from the continent as a whole. Again, investors’ interest was concentrated in SADC where more than 3,200 deals of $1.25 trillion from Africa were reported. Interestingly, the volume of capital inflow from outside Africa focused on COMESA. Across all RECs, investments centralized in the financial and business services sectors (as reflected by # of deals) while the coal, oil, gas, and metals sectors received the most capital.

MAIN TAKEAWAY

The experience of WAEMU shows that the formal establishment of a free trade (and single currency) regime alone does not automatically imply an increase in economic activity across member countries. We found that WAEMU-internal and Africa-wide trade has remained relatively limited. This is likely because other serious barriers continue to exist beyond those impacted by trade terms and a shared currency, including the well-documented lack of necessary logistical networks, and streamlined procedures for customs in the region. The insecurity in border areas, for example in Eastern Burkina Faso’s area close to Togo and Benin, has also become a major concern that is hindering smooth transportation in the area22. It is commendable that regional communities and trade facilitation agreements have formed and continue to exist across the continent. But these agreements are not sufficient to increase trade and investment on their own. This is true for both internal trade and investment within the community and the ability of the community to attract transformative business investment from outside. This suggests that larger trade agreements like AfCFTA may lead to limited impact only if negotiated policies and terms that aim to facilitate trade and capital flows lack a system of strict enforcement and external circumstances, such as infrastructure and security, remain unfavorable23.

Julia Conrad is currently pursuing a Master in Public Administration degree at Harvard Kennedy School (2023). Previously, she worked for five years at the International Finance Corporation (World Bank Group) in Dakar (Senegal), where she managed a portfolio of micro- and agriculture finance projects across Africa. Her studies at Harvard have focused on Infrastructure Development, Development Policy, and Climate Change. She also has a BSc in International Economics from the University of Tuebingen and a MEc in World Economics from the University of Finance and Economics in Shanghai.

———————–

1Website of the West African Economic and Monetary Union. “About UEMOA.” http://www.uemoa.int/en/about-uemoa(last visited: 23 July 2022)

2Website of the Economic Community of West African States. “Member States.” https://ecowas.int/?page_id=381 (last visited: 23 July 2022)

3 Britannica Online Encyclopedia. “Economic Integration.” https://www.britannica.com/topic/economic-integration(last visited: 23 July 2022)

4 Frankel, Jeffrey A. & Andrew K. Rose. “Estimating the Effect of Currency Unions on Trade and Output.” Quarterly Journal of Economics CXVII, 2 (May 2002): 437-466. https://www.nber.org/papers/w7857(last visited: 23 July 2022)

5Glick, Reuven & Andrew K. Rose. “Does A Currency Union Affect Trade? The Time-Series Evidence.” European Economic Review, 2002, v46 (6 June): 1125-1151. https://www.nber.org/papers/w8396 (last visited: 25 July 2022)

6 Micco, Alejandro, Ernesto Stein, Guillermo Ordoñez, Karen Helene Midelfart & Jean-Marie Viaene. “The Currency Union Effect on Trade: Early Evidence from EMU.” Economic Policy 18, no. 37 (2003): 317–56. http://www.jstor.org/stable/1344738 (last visited: 25 July 2022)

7 Pilling, David. “A revolution in Africa’s relations with France is afoot.” Financial Times. 31 December 2019. https://www.ft.com/content/8894ad6e-2650-11ea-9a4f-963f0ec7e134 (last visited: 25 July 2022)

8 Website of the West African Economic and Monetary Union. “The Amended Treaty.” http://www.uemoa.int/en/amended-treaty(last visited: 25 July 2022)

9 Ouattara, Alassane D. “The West African Economic and Monetary Union (WAEMU) – Facing the Challenges of the Future.” IMF. 30 June 1998. https://www.imf.org/en/News/Articles/2015/09/28/04/53/sp063098(last visited: 25 July 2022)

10Pangea Risk. “Special Report: Africa’s Common Markets Compete for Trade and Investment.” 8 March 2021. https://www.pangea-risk.com/wp-content/uploads/2021/03/SPECIAL-REPORT-AFRICAS-COMMON-MARKETS-COMPETE-FOR-TRADE-AND-INVESTMENT.pdf(last visited: 25 July 2022)

11Samba Sylla, Ndongo. “Moving forward to African Monetary Integration.” Africa Development/Afrique et Développement, 2020, Vol. 45, No. 2 (2020): 39-58. https://www.jstor.org/stable/26979255(last visited: 25 July 2022)

12 Pilling, David. “A revolution in Africa’s relations with France is afoot.” Financial Times. 31 December 2019. https://www.ft.com/content/8894ad6e-2650-11ea-9a4f-963f0ec7e134(last visited: 25 July 2022)

13Mieu, Baudelaire. “France begins transfer of €5bn to BCEAO as part of CFA franc reform.” The Africa Report. 5 May 2021. https://www.theafricareport.com/85566/france-begins-transfer-of-e5bn-to-bceao-as-part-of-cfa-franc-reform/ (last visited: 25 July 2022)

14 Wilson, James. “The CFA franc reforms are more symbolic than transformative.” LSE Blog. 19 March 2020. https://blogs.lse.ac.uk/africaatlse/2020/03/19/cfa-franc-reforms-monetary-policy-symbolic-colonialism/ (last visited: 25 July 2022)

15 Mugabi, Isaac. “West Africa’s Eco currency plan remains a pipe dream.” Deutsche Welle (DW). 2 July 2021. https://www.dw.com/en/west-africas-eco-currency-plan-remains-a-pipe-dream/a-58136111 (last visited: 25 July 2022)

16Ogbalu, Mike III. “Boosting the AfCFTA: The role of the Pan-African Payment and Settlement System.” Brookings. 11 February 2022. https://www.brookings.edu/blog/africa-in-focus/2022/02/11/boosting-the-afcfta-the-role-of-the-pan-african-payment-and-settlement-system/ (last visited: 25 July 2022)

17 Wikipedia. “CFA franc.” https://en.wikipedia.org/wiki/CFA_franc#cite_note-2020_nzaou_kongo-1 (last visited: 25 July 2022)

18Daan Freeman, Dean, Gerdien Meijerink & Rutger Teulings. “Trade benefits of the EU and the Internal Market.” CPB Netherlands Bureau for Economic Policy Analysis. January 2022. https://www.cpb.nl/sites/default/files/omnidownload/CPB-Communication-Trade-benefits-of-the-EU-and-the-Internal-Market.pdf (last visited: 25 July 2022)

19Website of the BCEAO. “Member States.” https://www.bceao.int/en/etats-membres (last visited: 25 July 2022)

20One must note that differences of income level are enormous REC-internally. For example, in COMESA and SADC, the Seychelles’ GDP per capita (current $) was more than 34-times that of Mozambique. In ECCAS, Equatorial Guinea’s per capita GDP was even than 37-times that of Burundi.

21Retrieved from The Atlas of Economic Complexity. The Growth Lab. Harvard Kennedy School of Government. https://atlas.cid.harvard.edu/explore?country=undefined&product=5895&year=2019&productClass=HS&target=Product&partner=undefined&startYear=undefined (last visited: 25 July 2022)

22 Salau, Sulaimon. “Poor infrastructure, insecurity hinder cross-border trade.” The Guardian. 8 May 2022. https://guardian.ng/business-services/poor-infrastructure-insecurity-hinder-cross-border-trade/(last visited: 25 July 2022)

23USAID. “West Africa Regional: Economic Growth and Trade.” Last updated 21 July 2022. https://www.usaid.gov/west-africa-regiona/economic-growth-and-trade (last visited: 25 July 2022)

A Free Trade Agreement Across the African Continent: Where Are the Export Opportunities for Nigeria?

After being fully implemented, the African Continental Free Trade Area (AfCFTA) is going to be the biggest Free Trade Agreement (FTA) ever in population and geographical size: more than fifty countries have been working since 2015 on tariff reductions in goods, rules of origin and procedures, technical barriers, or trade-in services, just to mention some topics. Considering that intra-regional trade is only 17% of total African exports (compared to 59% in Asia or 69% in Europe)1, this FTA could be a big step toward the goal of increasing exports (including diversification and more complex products) between African countries.

However, if we want to know where the export opportunities for a particular country are, it is hard to know where to start. The Agreement includes and addresses so many topics and issues that are easy to get lost. For instance, what are the binding constraints to intra-regional trade in practice and how is the AfCFTA going to impact them? Are those binding constraints the same for every sector in each country? What is the current situation in terms of tariffs and non-tariff barriers and how is that going to change?

I spent eight weeks trying to find an answer to these questions for Nigeria as part of a research sprint with Harvard’s Growth Lab. I analyzed the tariffs that Nigerian firms face when trying to export to other African partners. The main idea was to find and identify products where Nigeria might have comparative advantages in productive capabilities and where the other countries are currently imposing high import tariffs that the AfCFTA is going to reduce. Let’s go.

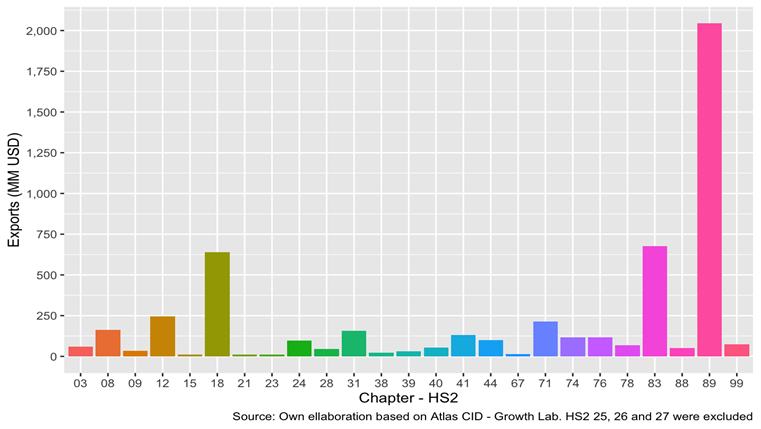

Nigeria mainly exports oil derivates (see Figure 1), and in those chapters (2-digit level of the Harmonized System (HS)) where exports were relatively high in 2019 (see Figure 2), we do not see very promising stories. In chapter 89 — which represents ships, boats, and floating structures — exports are mainly scrap vessels. In chapter 83, the data is just capturing a sporadic and unique export of metal articles that occurred in September 2019 and were not repeated in any other year. In chapter 18, we only find exports of raw or roasted cocoa beans with no further industrial processes.

Figure 1: Nigeria’s exports by sector

Figure 2: Nigeria’s exports in 2019 by Chapter (HS 2)

Therefore, for Nigeria, we need to dig deeper to look beyond the exports that dominate current trade and to those that might be nascent now but represent strategic growth opportunities. To find products with potential export opportunities we need to develop a systematic methodology that could be applied to every HS chapter. To develop such an approach, I take advantage of a detailed dataset that includes every import tariff that Nigeria is paying when trying to export to African countries.

Nigeria is part of ECOWAS, a custom union composed of 15 countries2, so for these countries, Nigeria is already paying 0% of import tariff. However, for the rest of the countries, the average levels are considerably high, as shown in Figure 3.

Figure 3: Tariff faced by Nigeria when exporting, Simple and Weighted (Exports 2019) Average

Considering that Nigerian exporters face high tariffs in some countries, a natural question arises: which products are going to have the highest tariff reduction? Additionally, it is useful to focus on products that have two characteristics: (1) they are being exported somewhere by Nigeria (let’s say, exports were higher than USD 3 MM in 2019), and (2) they faced a high average tariff (let’s say higher than 20%). Figure 4 shows products along these two dimensions.

Figure 4: Nigeria’s Total Exports and Tariffs faced in African Countries (excluding ECOWAS)

If we focus our attention on those products that have these characteristics, we find 10 products where Nigerian exporters would be likely to benefit from the FTA. These represent perhaps the clearest opportunities to increase exports on the intensive margin. Let’s look at some of these products, for example, crustaceans and beers, to understand the opportunity space better.

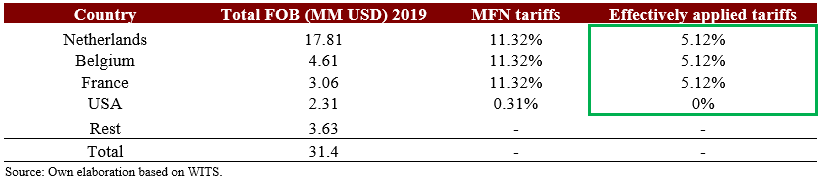

In the first case, a quick analysis in Table 1 shows us that Nigeria is exporting more than 90% of its crustacean exports to European countries, and that the effectively applied tariff in those countries is around 5%, while the average tariff to export to African countries is greater than 20%. Considering that Nigeria is the second-largest producer of farmed fish in the continent, and that many businesses are small and medium firms, it would be relevant to understand what type of characteristics the exporting firms share and how they succeeded in obtaining the required certifications to access into markets with high-quality standards such as the European Union or the US. On the other hand, the current production in Nigeria seems to be lower than its local demand. Therefore, to increase exports to African partners, Nigeria would seem to have to increase the local production3.

Table 1: Total Nigeria’s Exports 2019 of Crustaceans (HS4 0306)

The second case, beer, is quite different. As shown in Table 2, Nigeria exports to countries with 0% of applied tariff but also to Cameroon, which represents more than 20% of exports but where the tariff is 30%. This is in line with the average tariff across all the African countries, 26%. How is Nigeria successfully exporting to Cameroon even when the applied tariff is so high? How many firms are exporting beer to Cameroon? Is the tariff reduction going to incentivize more exports? To answer these questions, it would be indispensable to better understand the business profile and perspectives of the largest companies, like Nigerian Breweries.

Table 2: Total Nigeria’s Exports 2019 of Beer (HS4 2203)

The same analysis for the other 8 headings also gives interesting results. In general, Nigeria is currently exporting these products to countries with low tariffs, so it is possible that the AfCFTA could increase export opportunities in those products (and perhaps in other goods that are not being exported due to high tariffs and we are not detecting in our exercise).

This analysis is my first attempt at combining data from current exports and import tariffs in a systematic way to identify where export opportunities could be. The cutoff could be modified (1 instead of 3 MM, or 15% instead of 20% of import tariff), and one could also study or analyze the imports of the other African countries to better understand Nigeria’s role in those markets and the potential advantage that Nigeria could have with the AfCFTA compared to other exporters.

Since we are just using import tariffs and trade data, we must continue asking questions and exploring other trade aspects, such as non-tariff barriers or rules of origin and procedures or studying specific industries that could get positive and significant gains with the Agreement. Analyses like this are nevertheless important because within the complex spaced of trade and industrial policy in the context of new developments, like AfCFTA, it is often difficult for policymakers and other stakeholders to know where to start looking for opportunities.

A key advantage of this approach is that it can be easily repeated in any other African country, and by using it we can get initial ideas of which industries (in each country) could benefit through AfCFTA in terms of tariff reductions, and therefore inform local strategies in support of local businesses.

1See https://www.brookings.edu/blog/africa-in-focus/2019/02/22/figures-of-the-week-increasing-intra-regional-trade-in-africa/

2Benin, Burkina Faso, Cabo Verde, Cote d’Ivoire, The Gambia, Ghana, Guinea, Guinea-Bissau, Liberia, Mali, Niger, Nigeria, Senegal, Sierra Leone, and Togo.

3See https://www.feedstrategy.com/africa/nigerian-state-attracts-fish-farming-investors/

Enzo Dominguez Prost is currently pursuing a master’s degree at Harvard Kennedy School (MPA/ID, expected graduation in May 2023). Previously, he worked in Argentina for five years in the Ministry of Production on topics related to industrial policy and international trade. He has a BA (2012-2015) and a MA (2016) in Economics from “Universidad de San Andrés” (Argentina).

Namibia’s Diversification Strategy: Finding A Way Forward

Namibia is a country of 2.5 million people that gained independence from South Africa in 1990 and shares a legacy of apartheid that informs the socio-spatial distribution of its citizens. Its economy is highly reliant on the exports of a few primary commodities, such as minerals like diamonds, copper, uranium, gold, and zinc, and agricultural goods like fish and livestock. The mineral economy drives much of the growth of the country. Similar to my country, Peru, Namibia had a period of high growth during the commodity boom (2002 – 2015) but is now facing a growth challenge because of exogenous shocks such as falling commodity prices and COVID-19.

The Growth Lab is supporting the Government of Namibia (GoN) in the quest of finding new growth drivers that promote inclusive development. The project covers a wide range of research activities, such as: understanding the drivers of macroeconomic sustainability, diagnosing the constraints to growth and identifying the most binding structural barriers preventing Namibia from realizing sustainable growth and diversification opportunities, studying inequality and labor market dynamics across the country, and analyzing the economic and export diversification opportunities by applying the framework of complexity analysis. A key objective is leveraging the existing capital-intensive industries (i.e., minerals) to set the basis for productive diversification towards industries that can employ more people with higher capabilities and jumpstart the Namibian economy.

Although productive diversification and inclusion are shared goals, there are different approaches being considered to foster these new opportunities. On the one hand, the GoN has consistently promoted “beneficiation” since 2012 through its homegrown agenda. The beneficiation, or value-added, strategy focuses on adding more value downstream to current exports. On the other hand, the Growth Lab sees productive transformation as focusing on sectors that are “similar” in terms of skills and capabilities because of the shared knowhow required in the production process. These opportunities are (i) implicitly revealed through production and export data – i.e., like the product space; and (ii) not necessarily along the lines of vertical value chains, which might seem unintuitive at first glance. Put simply, while many governments believe that a strategy to diversify should go from cotton to textiles, the Growth Lab finds evidence of an optimal strategy that may go from cotton to fruits or coffee. “Similarity” is better understood through knowhow in the production process rather than vertical value chain integration.

Nonetheless, the idea behind beneficiation is intuitive and appealing to an economic-political messaging about “doing more at home.”It is an appealing idea for many reasons: saving on transportation costs as well as secured and cheaper local supply, and domestic import substitution. It also supports a sense of national pride by promoting the notion that employment and skills “evolve” downstream to higher-value products. Moreover, in a country with a dependence on commodities, adding value is also seen as an option to reduce exposure to the volatility of the international markets (i.e., selling batteries is less volatile than selling copper).

However, the Growth Lab has empirical evidence proving that countries do not transform by adding more value to their existing exports down the value chain. Klinger et al (2008) assess the effectiveness of beneficiation by analyzing international trade data for 200 countries over the previous 50 years. The conclusions – which are aligned with the economic literature on the same topic – is that countries do not transform by adding more value to their existing exports down the value chain. Instead, countries accumulate productive capabilities, redeploy, and recombine them into larger sets of more sophisticated products and services. Hence, beneficiation is likely to be unsuccessful.

My role in the Namibia project during the internship largely consisted in creating a new dataset using Namibia’s trade data to identify and compare the two approaches to industrial diversification. Based on Klinger et al (2008), I worked on the analysis, refined it with members of the team and external experts, and then presented my work to the counterparts. My findings were used in the policy recommendations made by the Growth Lab team to the Government of Namibia.

These are just a few highlights of what I learned:

- Analysis is a stronger piece of evidence than intuitive arguments: During my internship, I helped advance the agenda by identifying the top 50 industries that should be prioritized following a beneficiation strategy, and preparing a graph that contrasted them vis-à-vis the industries identified in the economic complexity report within the same product space. The graph showed how beneficiation is “as good as random”: the prioritized industries require different sets of capabilities and can differ greatly from Namibia’s existing industries. The visual contrast between both strategies made a stronger point than any theoretical discussion.

- History matters, context matters, and public perception matters: In the MPA/ID program, we learn that policies are not just about what is technically correct. One must take into account political and administrative feasibility. Given the historically salient role of beneficiation in the country, and in the broader South African Development Community, it was politically complex to expect a full shift out from beneficiation, so the team proposed a “middle ground” strategy: following capabilities first, then beneficiating if that’s in the optimal set. Some products in the plastics and rubbers product group fit these criteria since they were both directly downstream and in line with the existing set of capabilities.

- It matters not only when assessing policy recommendations, but also when thinking about the messages we want to convey: In Namibia, the Growth Lab recognized that we were outsiders to the country and that our message could be perceived as though we believed that the country was not capable of adding value to its existing industries. Thus, we looked for examples of industries where Namibia currently adds value to imported products (i.e., copper) to make the point that we do believe they are able to add value, but that it did not necessarily have to be to domestic products.

- Every good idea on paper leads to a lot of effort to implement them in order for them to materialize: Many policy recommendations sound reasonable on paper but fail to delve into how policymakers can actually “make it happen” given the existing organizational capacity and institutional setup. To address this natural gap in going from ideas to action, the Growth Lab facilitated the introduction of productivity taskforces and developed a framework of best practices to show how policymaking could be implemented to reduce coordination failures that constrain diversification efforts. As part of this process, we met with counterparts in the GoN to first understand similar efforts in the past to set up such taskforces and we incorporated those learnings into our recommendations.

- You cannot pursue single policies in isolation of other policy priorities. They have to complement each other. Fiscal sustainability and industrial policy had to go hand-in-hand: While diversification is a way of addressing Namibia’s growth and inclusion challenges, the team was also very aware of the fiscal constraints that the GoN currently faces. To that end, we argued that a beneficiation strategy was likely to require more fiscal resources given the big push needed to develop new capabilities. Similarly, a key best practice for the implementation of productivity taskforces is that they should not focus on measures that increase profits for firms (i.e., tax benefits), but on measures that help increase overall productivity.